How to Improve Credit Score Fast (2026 Guide)

From 612 to 720 — proven strategies that actually work.

No “credit repair” company can remove accurate negative information. Only time and consistent positive behavior improve your score. Equifax, Experian, and TransUnion update your file when lenders report (usually monthly).

2026 context: Average FICO score is 718. But 26% of Americans have scores below 670 (“subprime”), costing thousands in extra interest.

The reality: A single late payment can drop your score 50–100 points. But with the right strategies, you can gain 100+ points in 6–12 months — without paying a dime to a repair company.

You check your credit score. It’s 612. A mortgage? Denied. Car loan? 18% interest. Credit card? Secured only.

You feel stuck. But here’s the truth: improving your credit score is not a mystery. It’s a formula. Once you understand the five FICO factors, you can hack the system legally and ethically.

Over the next 5 minutes, I’ll show you exactly how to improve your credit score — the 2026 edition. No gimmicks. No “secret tricks.” Just strategies that have helped readers boost their scores by 100+ points.

- Payment history is 35% of your score. One late payment hurts more than anything else. Automate everything.

- Credit utilization is 30%. Keep balances below 10% of your limits for maximum points.

- Don’t close old credit cards. Length of credit history is 15% — the older, the better.

- Hard inquiries stay 2 years but only hurt for 12 months. Rate-shop within a 14–45 day window to count as one inquiry.

- Get free weekly reports at AnnualCreditReport.com — a right made permanent after COVID.

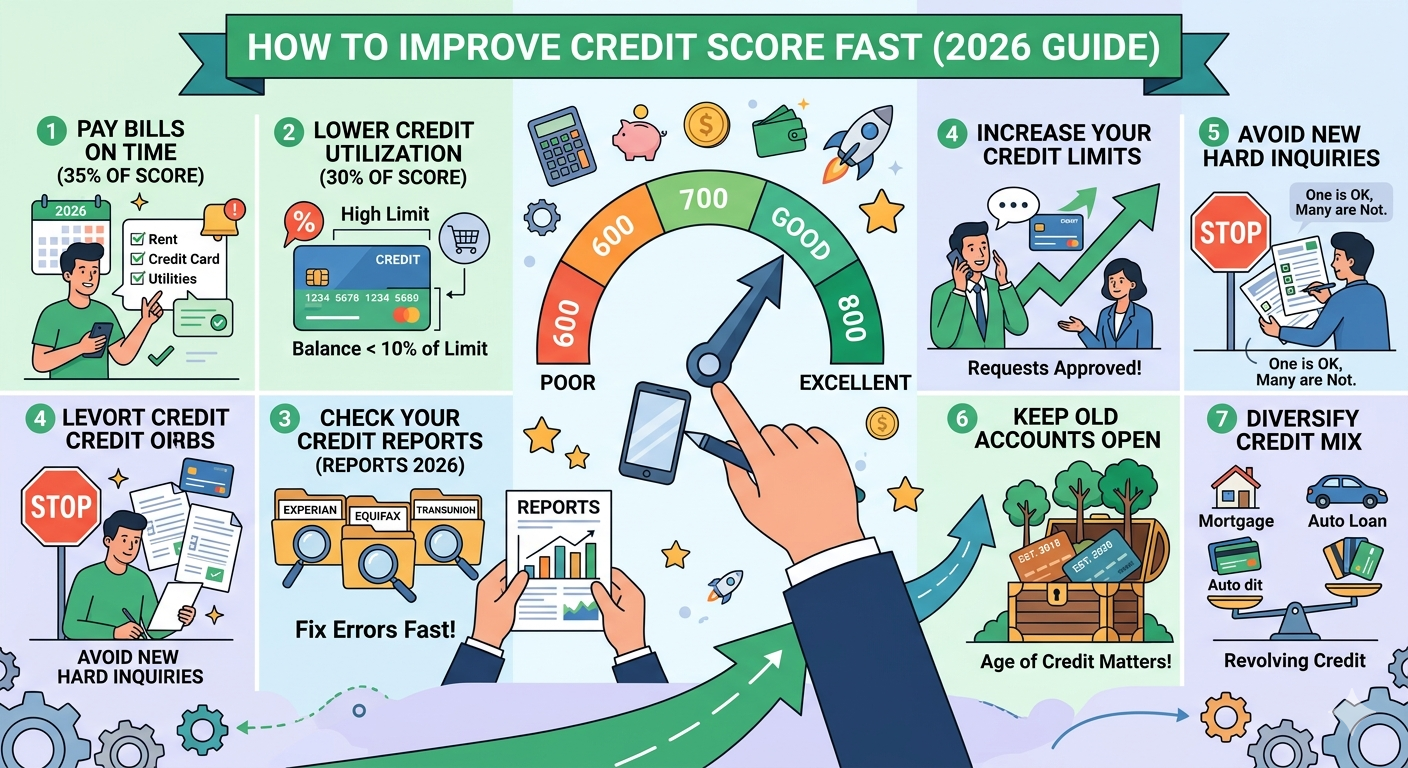

How Credit Scores Actually Work (The FICO 5)

Your FICO score (used by 90% of lenders) is calculated using five categories. Think of them as levers.

1. Payment History (35% — Most Important)

Late payments stay on your report for 7 years. Impact: 30 days late = -50 to -100 points; 60 days = additional drop; 90+ days (charge‑off) = -150+ points.

The fix: Never miss a payment. Set up autopay for at least the minimum due.

2. Amounts Owed / Credit Utilization (30%)

Utilization = total balances ÷ total limits. Keep it under 10% for excellent scores.

The fix: Pay down balances aggressively. Make multiple payments per month to keep reported balances low.

3. Length of Credit History (15%)

Older accounts help you. Never close old cards (unless high annual fee).

4. Credit Mix (10%)

Revolving (cards) + installment loans (mortgage, auto) is ideal.

5. New Credit / Hard Inquiries (10%)

Rate shopping within 14–45 days counts as one inquiry. For credit cards, each application is separate.

Credit Score Ranges and What They Mean (2026)

| Score Range | Rating | Avg Auto Loan Rate | Avg Mortgage Rate |

|---|---|---|---|

| 800–850 | Exceptional | 5.2% | 6.1% |

| 740–799 | Very Good | 6.1% | 6.5% |

| 670–739 | Good | 7.8% | 7.0% |

| 580–669 | Fair / Subprime | 11.5% | 8.5%+ |

| 300–579 | Poor | 14%+ | Often denied |

Rates are estimates for April 2026. Actual rates vary by lender.

Use our Credit Score Simulator to model the impact of paying down debt, opening a new card, or disputing an error. Enter your current score and debts — we’ll show your potential score in 3, 6, and 12 months.

The 7 Most Effective Ways to Improve Your Credit Score

1. Pay Every Bill on Time — Always

Autopay for minimum due + calendar reminder to pay full balance. Use Experian Boost or UltraFICO to add rent/utility payments.

2. Lower Utilization to Under 10%

Pay before statement closing date. Request credit limit increases every 6–12 months.

3. Become an Authorized User

Ask a trusted family member with excellent credit to add you to their oldest card. Instant history boost (+50 points possible).

4. Dispute Credit Report Errors

One in five reports has an error. Pull free weekly reports at AnnualCreditReport.com. Dispute online — bureaus must investigate within 30 days.

5. Pay Down High-Interest Debt Strategically

Avalanche (highest interest first) or snowball (smallest balance first). Focus on cards with highest individual utilization.

6. Get a Secured Card or Credit-Builder Loan

Deposit $200–$1,000 for a secured card. Use for small purchases, pay in full. Credit unions offer credit-builder loans.

7. Keep Old Accounts Open

Closing a card removes its limit and eventually its history. Keep open with a small recurring charge (Netflix) paid automatically.

Make two payments per month: 15 days before statement closing date (pay down to under 10% utilization), then 3 days before due date (pay remaining balance). This reports low utilization to bureaus while avoiding interest. Example: $10k limit, $2k spend → pay $1,500 early → $500 statement balance (5% utilization) → score boost.

Common Mistakes to Avoid

1. Closing Cards After Paying Them Off

You lose the credit limit and eventually the history. Keep it open, use once every 6 months.

2. Applying for Multiple Cards at Once

Each hard inquiry costs ~5 points. Space applications by 6–12 months.

3. Ignoring Medical Collections

Paid medical collections no longer appear. Unpaid under $500 ignored. Over $500 still hurts — negotiate before collections.

4. Paying for “Credit Repair” Services

No one can remove accurate negatives. Dispute errors yourself for free.

5. Never Checking Your Own Score

Checking your own credit is a soft inquiry — never hurts your score. Check weekly for free.

How Long Does It Take to Improve Credit Score?

| Action | Typical Increase | Timeframe |

|---|---|---|

| Pay a 30-day late payment current | +20–50 points | 1–2 months |

| Lower utilization from 90% to 10% | +50–100 points | 1 statement cycle |

| Become authorized user | +30–80 points | 1–2 months |

| Dispute an error | +10–50 points | 30–45 days |

| Open a secured card (no history) | +50–100 points | 6–12 months |

| Pay for delete (collection) | +50–150 points | 1–3 months |

Realistic timeline: 100 points in 6 months is achievable. Moving from “fair” (650) to “good” (720) typically takes 9–12 months.

Frequently Asked Questions (People Also Ask)

Q: How can I raise my credit score 100 points in 30 days?

A: Rare. Fastest legitimate ways: become an authorized user (+50), dispute major errors (+50), pay utilization from high to under 10% (+50). But 100 points in 30 days usually requires removing errors or collections.

Q: Does checking my credit score lower it?

A: No. Soft inquiries never affect your score. Only hard inquiries from applications matter.

Q: How long do late payments stay on credit reports?

A: 7 years from the late date. Impact fades over time.

Q: Does paying off a collection remove it?

A: Not automatically. Paid collections stay for 7 years. Ask for “pay for delete” in writing before paying.

Q: Can I get a mortgage with a 620 credit score?

A: Yes — FHA loans accept 580 with 3.5% down. Conventional loans usually require 620 minimum, but rates will be higher.

Q: How many points does a hard inquiry cost?

A: Typically 3–5 points. Fades after 6 months, gone after 12 months.

Q: What’s a good score to buy a car?

A: 660+ for standard rates, 720+ for best rates. Below 600 expect high rates or a cosigner.

Q: Does rent affect credit score?

A: Not automatically. Use Experian Boost or Rental Kharma to report rent. Only missed rent sent to collections hurts.

Q: How often should I check my credit report?

A: At least quarterly. Free weekly at AnnualCreditReport.com through 2026. Stagger requests — one bureau every 4 months.

Q: Can I freeze my credit to prevent fraud?

A: Yes, free with Equifax, Experian, TransUnion. Freeze prevents new accounts. Thaw temporarily when applying for credit.

Final Verdict

Improving your credit score is not complicated — but it requires discipline and patience.

Three fastest actions you can take today:

- Check your credit reports for errors and dispute them immediately.

- Pay down credit card balances to under 10% of your limits.

- Ask a trusted family member to add you as an authorized user.

Three long-term habits for excellent credit:

- Autopay everything — never miss a due date.

- Keep old accounts open — age is your friend.

- Apply for credit sparingly — only when you need it.

The Golden Rule: Your credit score measures how reliably you repay debt. Every on-time payment builds trust. Every late payment erodes it. There are no shortcuts — only consistent, responsible behavior.

Your next step: Pull your free credit reports today. Find one error or one high-utilization card to fix. Take that single action within the next 24 hours. In 6 months, you won’t recognize your score.