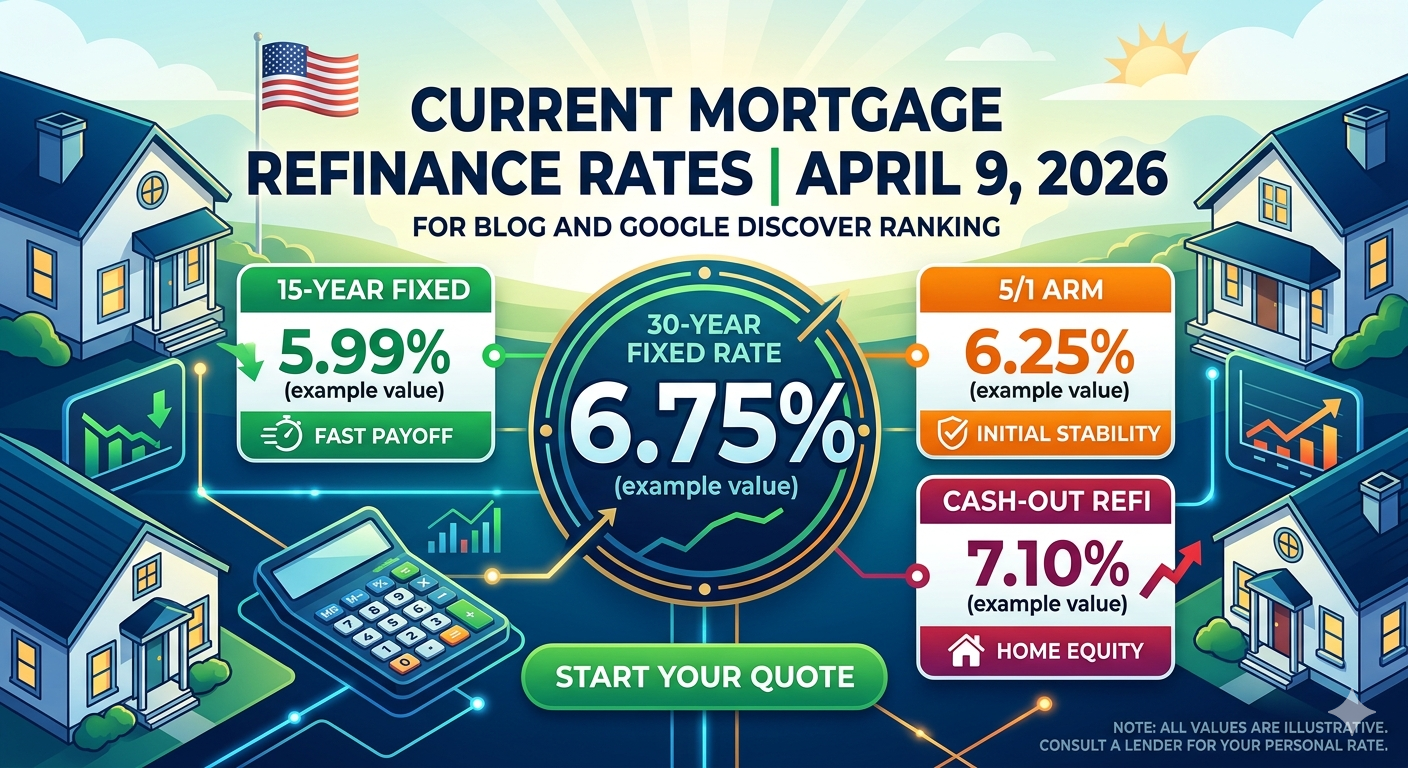

Current Mortgage Refinance Rates as of April 9, 2026

The average mortgage refinance rate is on the decline. This includes rates for 15-year and 30-year fixed rates. The spring rate slowdown means that rates for potential homeowners are lower than in March. For homeowners who are looking to refinance, they can expect rates to be even lower than a few months ago.

The Refinance Rates: A Key Component – April 9, 2026

These figures, which are as of April 9, 2026, are predicted by the latest Bankrate, Freddie Mac and Mortgage Bankers Association surveys. However, these average rates can be affected by factors such as credit scores, lender considerations and loan-to-value ratios.

| Loan Type | Interest Rate | APR (Estimate) |

|---|---|---|

| 30-Year Fixed Refinance | 6.57% – 6.74% | 6.76% – 6.83% |

| 20-Year Fixed Refinance | 6.51% | 6.62% |

| 15-Year Fixed Refinance | 5.68% – 5.98% | 5.93% – 6.10% |

| 10-Year Fixed Refinance | 5.92% – 6.21% | 5.98% – 6.06% |

| 5/1 ARM Refinance | 6.07% | 6.18% |

| 30-Year VA Refinance | 6.50% | 6.54% |

| 30-Year Jumbo Refinance | 6.79% | 6.84% |

Refinance rates are typically higher than average market rates by between 20 and 30 basis points. If you look at the 30-year fixed-rate mortgage average market rate, it is 6.51%, while the average refinance rate tends to be around 6.57%. This is because lenders view refinancing as a riskier option than other options. So don’t be surprised if you are not offered the same rate advertised for new purchases.

What Has Changed in Mortgage Refinance Interest Rates?

At the moment, there are three factors that influence refinance rates:

1. Geopolitical Tensions and Oil Prices

After the Iran war and the closing of the Strait of Hormuz, which is crucial for oil production, the price of crude is approaching $100 per barrel. Oil prices increase the cost of living which in turn increases bond yields, and eventually mortgage rates. Analysts predict rates will exceed 6.75% in the near future. David Kakish, mortgage consultant, explained that rates fell below 6% for the first time in over a year at the end of February. Then oil price inflation expectations grew, bond yields rose, and mortgage rates followed.

2. U.S. Treasury 10-Year Yields

Banks and lenders base their interest rates on the yield of 10-year U.S. Treasury bonds. The current yield is between 4.31% and 4.36%. At this point, a refinance is likely to be more common than a first mortgage.

3. Federal Reserve Policy

After the Federal Reserve cut rates at the end of 2025, it has kept its target for interest rates between 3.50% and 3.75%. Jerome Powell stated, “the bar is higher for cuts now,” which means that the federal funds rate will remain in the low-to-mid 6% range for a long period.

MBA Survey Shows Demand for Refinancing Has Dropped

According to the most recent MBA Weekly Mortgage Applications Survey published on April 8, 2026, for the week ended April 3, it paints a picture of a declining market:

- The Refinance Index fell by 3% compared to the week before, which represents a 4% annual decrease when comparing this week to last year.

- Since December 2025, the number of refinance applications submitted has decreased.

- The refinance share of total mortgage activity decreased from 45.3% to 44.3% from the week before.

- FHA applications increased 5% in the past week due to FHA’s rates which are approximately 30 basis points lower than conventional mortgages.

According to a recent analysis, the Refinance Index fell 17% over a period of ten days, indicating a sensitivity towards short-term interest rates. The Refinance Index is still 33% higher than last year’s levels due to structural demand from homeowners with loans below 4%.

Refinancing: Is It Worthwhile? The Math

A large number of homeowners are currently paying rates under 4% due to the pandemic refinance boom. This means that the current market rates for refinancing would be uneconomical for the majority. As long as interest rates are above 6%, it is rare for homeowners to refinance since they have rates below 5%.

You may be paying a higher rate than 7% if you locked in your mortgage in 2023 or early 2024. The current mortgage rates can offer real savings. The 15-year refinance rate is currently 5.68% – that’s a whole percentage point less than the mortgage rates in late 2023.

Refinancing should not follow the outdated “1% rule”. Refinancing decisions should not be based on a particular interest rate but rather analyzed to determine break-even. If closing costs are $4,500 and you save $200 per month, that translates to a break-even point of 22.5 months. You should plan on staying in the home for a period beyond this break-even point.

Expert Outlook: Where Are Rates Headed?

In the near future, it is likely that rates will remain stable or only slightly decrease. The Mortgage Bankers Association predicts that refinancing rates will stay between 6% and 6.5% through 2026. Fannie Mae predicts that rates will fall to 5.9% by the end of 2026. Morgan Stanley predicts that rates will drop in 2026 but then rise higher than they started. Experts advise against trying to predict interest rates as it almost always fails.

Practical Tips for April 9, 2026

For those considering refinancing:

- Run the numbers honestly. Calculate how long you intend to stay in the home after refinancing.

- Compare rates from different lenders. Rates can vary by as much as 0.5%.

- Consider a 15-year fixed refinance at 5.68% instead of a 30-year at 6.57% if you can afford higher monthly payments.

- A 5/1 ARM at 5.72% may be the better choice if you plan to sell or refinance within 5 years.

- Check your credit score. Even a small increase can make a big difference.

- If your current rate is below 6%, don’t refinance. The numbers don’t favor you.

- If you’re in the 6%–7% range, double-check the math on your break-even point.

- If you’re above 7%, you can likely save money. On a $400,000 loan, the difference between 7.25% and 6.50% is about $200 per month.

The Bottom Line

On April 9, 2026, refinance rates are in the high-to-mid 6% range. This is lower than the 8% rates seen in late 2023 but higher than the pandemic-era lows.

Waiting is the easy choice for many homeowners with rates below 4%. For those who purchased during the rate spike of 2023–2024, today’s market could offer a great opportunity to lower your monthly payments.

Stop trying to predict where markets will go. Refinance if the terms of the loan are favorable to your current situation. Be patient if they aren’t. The best refinance is the one which meets your goals – not one which chases the latest headline.